How to Pick the Right Payment Processor (Without Getting Burned by Hidden Fees)

Sam Reid · Senior Financial Markets Analyst

Staff Writer

Sam Reid · Senior Financial Markets Analyst

Staff Writer  28th Jun 2026

28th Jun 2026

Your payment processor is one of the most consequential vendors you’ll ever choose. Most business owners don’t realise that until something goes wrong: a declined transaction at checkout, a fee structure that quietly drains margin, or a contract that’s nearly impossible to exit. This guide cuts through the noise so you can make the decision once and make it well.

The Short Answer

A payment service provider (PSP) is a company that lets your business accept electronic payments. To pick the right one, you need to weigh five things: pricing model (flat-rate, interchange-plus, or tiered), total cost beyond the headline rate, how well it integrates with your existing setup, what fraud and chargeback protection looks like, and whether the contract terms give you room to leave if things change.

The rest of this guide explains exactly what each of those means and what to watch out for.

What Is a Payment Service Provider?

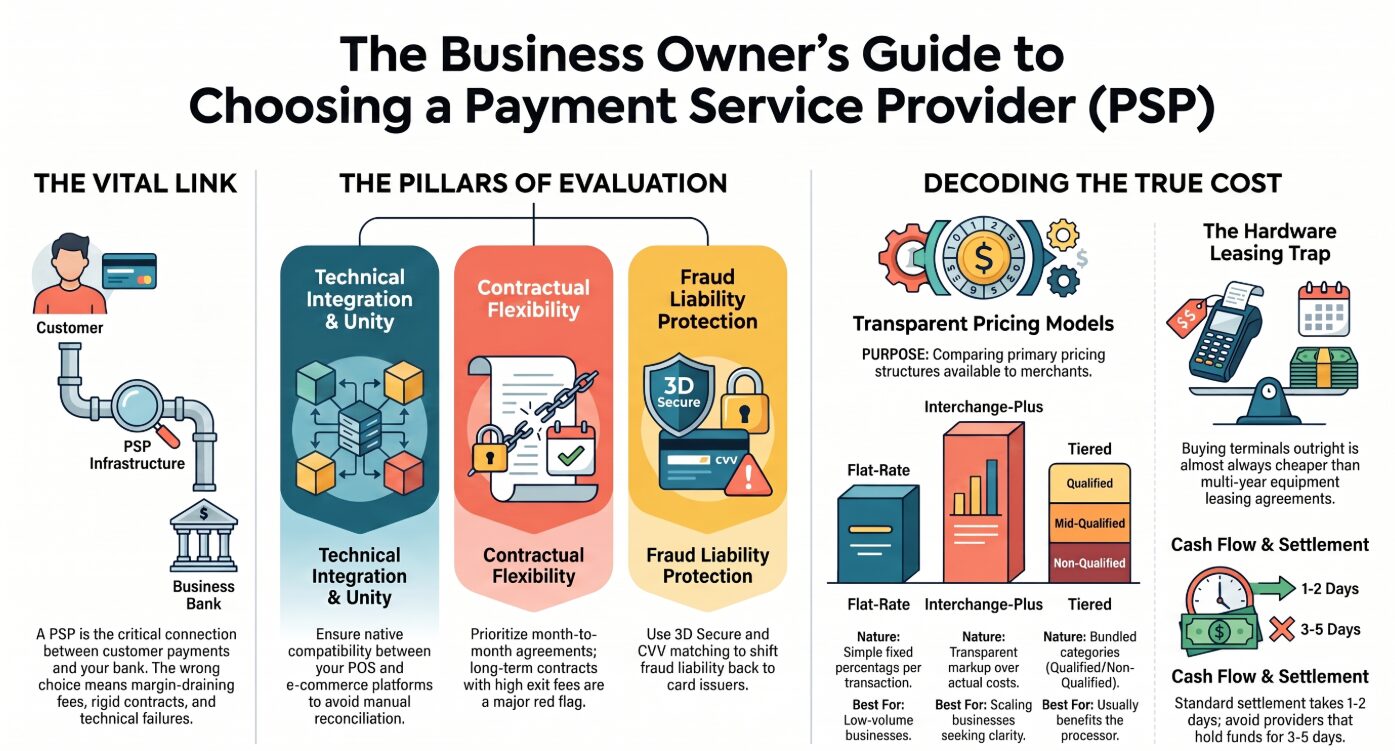

A payment service provider (PSP) is a company that lets businesses accept electronic payments, whether that’s credit cards, debit cards, bank transfers, or digital wallets. Think of it as the infrastructure layer between your customer handing over their card details and the money landing in your business account.

What makes the term slightly confusing is that it gets used to mean different things depending on context. Sometimes people use “payment service provider” and “payment processor” interchangeably. Other times, a PSP is described more specifically as a company that aggregates merchants under a single master account, rather than setting each business up with its own dedicated merchant account. Both uses are common. What matters for your purposes is understanding what the provider you’re evaluating actually does, and what that means for how you get paid.

There’s also a more technical definition worth knowing if you operate in Europe or are thinking about expanding there. Under the EU’s Payment Services Directive (PSD2), a payment initiation service provider (PISP) is a specific category of regulated provider that can initiate payments directly from a customer’s bank account, bypassing card networks entirely. PISPs operate under a separate licence and are part of the broader open banking framework. If you’re in e-commerce and considering account-to-account payment options, this is a category worth understanding.

So to answer the question directly: a payment service provider is any regulated company that facilitates the movement of money between buyers and sellers. That umbrella covers processors, gateways, acquirers, and PISPs, depending on which part of the transaction they handle.

What Payment Processing Actually Is (and Why It’s More Complex Than You Think)

When a customer taps their card, it feels instant. Behind that tap, a lot happens in under two seconds.

The transaction travels from your terminal or checkout page to a payment processor, which routes it to the relevant card network (Visa, Mastercard, and so on). The card network contacts the customer’s bank, which either approves or declines based on available funds and fraud signals. That approval travels back the same way, and the sale goes through. Settlement, when the money actually lands in your account, happens separately, usually one to two business days later.

This matters for one reason: every handoff in that chain has a cost, and those costs eventually land on you. Understanding the flow helps you understand the fees.

According to McKinsey & Company in 2023, the global payments industry handled 3.4 trillion transactions, accounting for $1.8 quadrillion in value and generating a revenue pool of $2.4 trillion. That’s the infrastructure your business plugs into every time someone pays you.

Payment Service Providers, Gateways, and Merchant Accounts: What’s the Difference?

These three terms get used interchangeably and they shouldn’t, because mixing them up leads to paying for services you already have.

A payment gateway is the technology layer that encrypts and transmits transaction data. In e-commerce, it’s what connects your website to the broader payment network. In-store, your card terminal usually handles this function.

A payment processor is the company that actually moves the money: routing transactions between banks, handling authorisation, and managing settlement. They’re the operational engine.

A merchant account is a specific type of bank account that holds funds after a transaction is approved, before they transfer to your regular business account. Some payment service providers bundle merchant account functionality into their service. Others require you to set one up separately with a bank.

Is a bank a payment service provider? Yes, technically, in that many banks offer merchant services and act as the acquiring bank in a transaction. But most businesses today don’t go directly to a bank for payment processing. They use a specialist PSP that handles the merchant account, gateway, and processing in a single package. Whether you’re better served by a bank-backed solution or a specialist PSP depends on your transaction volume, business type, and how much flexibility you need.

When comparing providers, find out what’s included. If a processor advertises low rates but doesn’t include gateway or merchant account services, you’ll pay additional fees elsewhere to fill those gaps.

The True Cost of Payment Processing

The rate a processor advertises is rarely what you actually pay. Here’s how the cost structure works.

Interchange fees are set by card networks, not your processor. They’re non-negotiable and vary based on card type, transaction method, and industry. Credit cards cost more to process than debit cards. Rewards cards cost more than standard ones. Card-not-present transactions (online or by phone) cost more than in-person ones.

Processor markup is what your PSP adds on top of interchange.

Below are different pricing models

- Flat-rate pricing charges a fixed percentage on every transaction regardless of card type. It’s simple, but often more expensive for businesses processing higher volumes.

- Interchange-plus pricing passes the actual interchange cost to you and adds a fixed markup on top. More transparent, often cheaper at scale, but harder to predict month to month.

- Tiered pricing bundles transactions into categories (typically “qualified,” “mid-qualified,” and “non-qualified”) with different rates for each tier. This model tends to benefit the processor more than the merchant, because most transactions quietly fall into the more expensive tiers. It’s worth scrutinising carefully before signing.

Beyond the processing rate, expect to see some combination of monthly fees, per-transaction fees, batch fees, and PCI compliance fees. Know what each one is before you commit.

The Hidden Costs Nobody Talks About

Chargeback fees apply every time a customer disputes a transaction, regardless of whether the dispute is valid. These typically run £15 to £50 per incident (or the dollar equivalent). If your chargeback ratio gets too high, your PSP can suspend your account or reprice your contract.

Early termination fees appear in contracts that lock you in for one to three years. Exit early and you could owe hundreds, or in some cases thousands, depending on the terms.

Equipment leasing costs look affordable month to month but often add up to far more than the hardware is worth over a two or three year term. Buy your terminal outright wherever possible rather than leasing it.

Refund fees catch most businesses by surprise. Some processors keep the original transaction fee even when a sale is reversed. You effectively pay to process a transaction you didn’t keep the revenue from.

Settlement timing is a softer cost but a real one. If your processor holds funds for three to five days as standard practice, that’s a consistent drag on cash flow, particularly for businesses running on tight margins.

What “Integration” Really Means for Your Business

A payment provider service that works technically isn’t the same as one that works well for your specific setup.

If you run a physical location, the processor needs to be compatible with your point-of-sale system. If you sell online, it needs to connect cleanly to your e-commerce platform. If you do both, you want a single system that unifies transaction data. Otherwise you’re reconciling two separate reports at the end of every month.

Ask directly: does this PSP integrate natively with your POS or platform, or does it require a third-party gateway to bridge the connection? Each additional layer is another monthly fee and another potential point of failure.

For businesses with custom-built systems, API quality matters. A well-documented, stable API means your development team can build reliable integrations. A poorly documented one means ongoing maintenance costs you didn’t budget for.

Security, Fraud Prevention, and What You’re Actually Liable For

PCI DSS (Payment Card Industry Data Security Standard) compliance is a requirement for any business that accepts card payments. Your payment service provider should handle the heavy lifting here, but you’re still responsible for maintaining compliance on your end. Non-compliance fees typically run £20 to £50 per month and can jump substantially if a data breach occurs.

For in-person transactions, make sure your setup supports EMV chip cards and contactless payments. Magnetic stripe transactions carry higher fraud liability that falls on the merchant, not the processor.

For online transactions, card-not-present fraud is the bigger risk. Look for PSPs that include address verification, CVV matching, and 3D Secure authentication. These don’t eliminate fraud, but they shift liability back to the card issuer when a properly verified transaction turns out to be fraudulent.

On chargebacks: understand your provider’s dispute management process before you need it. Some PSPs give you clear documentation tools and proactive alerts. Others leave you to figure it out yourself. The difference matters when you’re contesting a £3,000 transaction.

How Your Business Type Should Drive the Decision

Not every payment service provider fits every business. The right choice depends heavily on how you operate. High-volume retail or food service needs fast transaction speeds, reliable uptime, and hardware that holds up under constant use. Settlement speed and volume pricing matter more here than feature depth.

E-commerce priorities shift to gateway quality, fraud tools, and how the processor handles card-not-present risk. International payment support matters if any portion of your customers are outside the UK.

Subscription or SaaS businesses should look for built-in recurring billing tools, automated retries on failed payments, and flexible billing cycle options. Bolting these on through third parties adds cost and complexity.

High-risk industries, including certain categories in travel, gaming, supplements, and financial services, face a narrower pool of willing PSPs and higher rates. If your business falls into one of these categories, identify providers that explicitly work with your industry rather than discovering mid-application that you don’t qualify.

Businesses planning international expansion need to confirm which currencies and local payment methods are supported, what cross-border fees apply, and how funds settle across different markets.

Questions to Ask Before You Sign Anything

Most businesses skip this part. These are the questions worth asking before you’re locked in.

What is the full pricing model, and can you show me a sample monthly statement? Is there a contract, and what are the termination terms? What is the standard settlement timeline? How are chargebacks handled, and what does the dispute process look like in practice? What happens if my chargeback ratio exceeds your threshold? Is PCI compliance included or a separate fee? What support is available, and during what hours? Can this system scale with my transaction volume without triggering a reprice? Are there fees for refunds, failed transactions, or account inactivity?

A provider that can’t answer these questions directly before you sign is telling you something.

Red Flags That Should Make You Walk Away

Vague or verbal pricing. If the pricing isn’t clearly documented before you sign, that ambiguity isn’t an accident.

Long contracts with high exit fees. Month-to-month or short-term agreements are the norm with reputable providers. Multi-year lock-ins with steep penalties are not.

Tiered pricing without clear tier definitions. “Qualified” and “non-qualified” rates that aren’t explained upfront almost always mean more transactions land in the expensive tier than you expect.

Equipment leasing. Lease agreements on card terminals are almost always a bad deal over any period longer than 12 months. Buy the hardware.

Slow or unavailable support. If you can’t reach a human being during business hours before you’re a customer, assume it’ll be harder after.

Promised rates that require transaction volumes your business may not reach. Some PSPs advertise attractive rates tied to minimums that disqualify most of the businesses they’re marketing to.

How to Make the Final Call

Start with your current reality. What’s your monthly transaction volume? What’s your average transaction value? Are most of your sales in person, online, or split across both? Do you take payments internationally?

Run the maths on total cost, not just the headline rate. Take a recent month of sales and estimate what each shortlisted payment service provider would have actually charged you, including monthly fees, per-transaction fees, and any other line items that appear on a live statement.

Then think 18 months out. Is your volume likely to grow? If so, does the pricing model get better or worse at higher volumes? Are there features you don’t need today but will need as you scale?

The best payment service provider for your business isn’t the cheapest one or the one with the longest feature list. It’s the one whose pricing, contract terms, integration capabilities, and support model fit how you actually operate, today and over the next few years.

Compare at least three providers with that lens. The time you invest now is considerably less painful than unpicking a bad contract 18 months in.