CPI Explained: Why Inflation Data Moves the Markets

Sam Reid · Senior Financial Markets Analyst

Staff Writer

Sam Reid · Senior Financial Markets Analyst

Staff Writer  16th Mar 2026

16th Mar 2026

Every month, a single economic report sends shockwaves through global financial markets within seconds of its release. Stocks swing wildly, bond yields spike or plunge, and currency traders scramble to adjust positions. The culprit? The Consumer Price Index, a seemingly straightforward measure of how much Americans pay for everyday goods and services.

Understanding how inflation data moves markets isn’t just academic knowledge for economists. If you hold a retirement account, own bonds, or trade currencies, CPI releases directly affect your wealth. I’ve watched traders prepare for these announcements like surgeons before an operation: screens arranged, orders pre-loaded, fingers hovering over keyboards. The intensity exists because CPI figures shape everything from Federal Reserve policy to corporate profit expectations to the strength of the US dollar against every major currency on earth.

The disconnect between what CPI actually measures and how markets interpret it creates opportunities for informed investors and traps for everyone else. A 0.1% surprise in either direction can move trillions of dollars in asset values within minutes. Yet most retail investors barely glance at these releases, missing both the risks and the potential advantages that come from understanding what the numbers really mean.

The Fundamentals of the Consumer Price Index

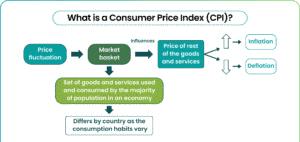

The Consumer Price Index represents the government’s attempt to measure what inflation actually feels like for ordinary households. Rather than tracking every transaction in the economy, the Bureau of Labor Statistics focuses on what typical urban consumers actually buy, from groceries to gasoline to healthcare services.

The index matters because it serves as the primary yardstick for measuring purchasing power erosion. When CPI rises 3% annually, your dollars buy roughly 3% less than they did twelve months ago. This affects everything from Social Security adjustments to union wage negotiations to inflation-protected bond payouts.

How the Bureau of Labor Statistics Calculates the Basket of Goods

The BLS doesn’t just pick random items to track. They survey approximately 24,000 households every quarter through the Consumer Expenditure Survey, asking detailed questions about spending patterns. This data shapes the “basket” of roughly 80,000 items tracked monthly across 75 urban areas.

The weighting system reflects actual spending habits. Housing costs represent about 33% of the index because that’s roughly what Americans spend on shelter. Food accounts for approximately 13%, transportation around 16%. When gas prices spike, the impact on CPI depends on how much weight fuel carries in the basket, not just the percentage change at the pump.

Price collectors visit stores and service providers monthly, recording actual transaction prices rather than advertised ones. The methodology includes quality adjustments: if a new smartphone costs the same as last year’s model but has better features, the BLS calculates an effective price decrease. This “hedonic adjustment” creates controversy, with critics arguing it understates true inflation experienced by consumers.

Headline vs. Core CPI: Why the Difference Matters

Headline CPI includes everything in the basket. Core CPI strips out food and energy prices. The distinction exists because food and energy prices swing dramatically based on weather, geopolitical events, and supply disruptions that don’t reflect underlying economic conditions.

Markets and the Federal Reserve often focus more heavily on core CPI because it better signals persistent inflation trends. A hurricane destroying Gulf Coast refineries might spike gas prices temporarily, but that doesn’t indicate the economy is overheating. Core inflation filtering out that noise reveals whether wage pressures, housing costs, and service prices are building sustained inflationary momentum.

The practical difference matters enormously. In 2022, headline CPI peaked above 9% while core remained closer to 6%. Traders watching only headline numbers might have expected more aggressive Fed action than actually materialized. Understanding which measure policymakers emphasize helps predict their actual responses.

The Direct Link Between CPI and Monetary Policy

Inflation data doesn’t just describe economic conditions: it actively shapes the policy response that determines borrowing costs across the entire economy. The Federal Reserve’s reaction function to CPI surprises creates the mechanism through which inflation numbers move markets.

Federal Reserve Mandates and Inflation Targets

Congress gave the Federal Reserve a dual mandate: maximum employment and stable prices. The Fed interprets “stable prices” as 2% annual inflation, measured by their preferred gauge, the Personal Consumption Expenditures index. However, CPI releases arrive earlier and more frequently, making them the market’s real-time signal for inflation trajectory.

When CPI runs hot, markets immediately price in higher probability of Fed rate hikes. The logic flows directly: higher rates make borrowing more expensive, which slows economic activity, which eventually reduces inflation pressure. Every 0.1% CPI surprise translates into basis point adjustments in expected future Fed funds rates.

The Fed’s 2% target isn’t arbitrary. Research suggests this level provides enough cushion above zero to give policymakers room for rate cuts during recessions while remaining low enough that households don’t factor inflation into daily decisions. When CPI persistently exceeds this target, the Fed faces pressure to act aggressively.

Interest Rate Projections and the ‘Dot Plot’

Four times annually, Fed officials publish their individual projections for future interest rates through the Summary of Economic Projections. The “dot plot” shows where each member expects rates to land over the coming years. CPI releases between meetings shift market expectations about how those dots will move.

A hotter-than-expected CPI print might push the median dot higher at the next meeting, signaling more rate hikes ahead. Markets don’t wait for official announcements: Fed funds futures immediately reprice to reflect updated expectations. This repricing cascades through every interest-rate-sensitive asset class simultaneously.

The relationship creates a feedback loop. If markets price in aggressive tightening after a high CPI print, financial conditions tighten before the Fed even acts. Mortgage rates rise, corporate bond spreads widen, and stock valuations compress. The anticipation of policy change becomes the policy change itself.

Why Stock and Bond Markets React to Inflation Surprises

The mechanical connection between CPI and Fed policy explains part of market reactions, but the full picture involves how inflation affects corporate profits and asset valuations directly.

Impact on Corporate Earnings and Profit Margins

Inflation creates both winners and losers among publicly traded companies. Businesses with pricing power can pass higher input costs to customers, protecting margins. Companies facing commodity cost increases without ability to raise prices see profits squeezed.

During the 2021-2022 inflation surge, consumer staples companies generally maintained margins while retailers with price-sensitive customers struggled. Energy companies benefited from rising oil prices while transportation firms faced higher fuel costs. Sector rotation following CPI releases often reflects these differential impacts.

The wage component matters particularly for service-intensive businesses. If CPI data suggests wage pressures are building, labor-intensive companies face margin compression expectations. Conversely, capital-intensive businesses with minimal labor costs might see relative outperformance.

Bond Yields and the Discounting of Future Cash Flows

Bond markets react to CPI through two channels: expected Fed policy and inflation expectations embedded in yields. When CPI surprises to the upside, bond prices fall as yields rise to compensate investors for both higher expected short-term rates and greater inflation erosion of future coupon payments.

The impact extends beyond bonds themselves. Stock valuations depend on discounting future earnings to present value. Higher discount rates, driven by higher yields, mathematically reduce the present value of those future earnings. Growth stocks with earnings weighted toward distant years suffer most when yields spike.

Treasury Inflation-Protected Securities provide a direct read on inflation expectations. The spread between TIPS yields and nominal Treasury yields, called the breakeven inflation rate, moves immediately on CPI releases. If the 10-year breakeven jumps from 2.3% to 2.5% following a CPI report, markets are signaling they expect higher average inflation over the coming decade.

Currency Volatility and the Global Ripple Effect

CPI data doesn’t stop at US borders. The dollar’s role as global reserve currency means American inflation figures move exchange rates worldwide, affecting international trade, emerging market debt, and commodity prices.

The US Dollar Strength and International Trade

Higher US inflation typically strengthens the dollar through the interest rate channel. If markets expect the Fed to raise rates in response to hot CPI data, higher US yields attract capital flows from lower-yielding currencies. The EUR/USD pair often moves 50-100 pips within minutes of significant CPI surprises.

For UAE-based investors holding dollar-pegged dirhams, this dynamic creates indirect effects. While the AED/USD rate remains fixed, a strengthening dollar against other currencies affects returns on European or Asian investments. An Irish-domiciled ETF tracking European stocks might decline purely from currency effects following a strong US CPI print.

Emerging market economies face particular vulnerability. Many hold dollar-denominated debt, and a strengthening dollar increases their repayment burden in local currency terms. Capital flight from emerging markets often accelerates following CPI-driven dollar strength, creating contagion effects across global equity markets.

Psychological Impacts and Consumer Sentiment

Beyond mechanical market effects, inflation data shapes consumer and business behavior through expectations channels. The University of Michigan Consumer Sentiment survey shows inflation expectations correlate strongly with actual spending decisions.

When consumers expect prices to rise, they may accelerate purchases, creating self-fulfilling inflation pressure. Alternatively, if inflation erodes real wage growth, discretionary spending suffers. Retail stocks often move on CPI releases based on these second-order effects on consumer behavior.

Business investment decisions similarly depend on inflation expectations. Companies facing uncertain input costs may delay capital expenditure, affecting industrial and materials sectors. The confidence channel through which CPI affects real economic activity sometimes matters more than the direct price effects.

Navigating Market Volatility on CPI Release Days

CPI releases occur at 8:30 AM Eastern Time, typically on the second or third Wednesday of each month. Experienced traders approach these mornings with specific preparation strategies.

Position sizing matters enormously. The potential for 1-2% equity index moves within minutes means overleveraged positions can face margin calls before traders can react. Many professionals reduce position sizes heading into releases or use options strategies to define maximum losses.

The initial market reaction often reverses partially within the first hour. Algorithmic trading systems react instantly to the headline number, but human traders analyzing the component details may reach different conclusions. The shelter component, medical care prices, and used car prices each tell different stories about inflation persistence.

For longer-term investors, CPI volatility creates opportunities rather than threats. If your investment thesis depends on fundamentals rather than monthly data points, price dislocations following CPI releases may offer attractive entry points. The key lies in distinguishing temporary volatility from genuine changes in economic trajectory.

Consider maintaining a watchlist of quality assets you’d buy at lower prices. When CPI-driven selloffs occur, you’ll have predetermined levels for action rather than making emotional decisions amid market chaos. This approach transforms monthly volatility from a source of anxiety into a systematic opportunity.

The relationship between inflation data and market movements will persist as long as central banks target price stability. Understanding the transmission mechanisms from CPI to Fed policy to asset prices gives you an edge over investors reacting purely to headlines. That edge compounds over time, turning monthly data releases from threats into opportunities for informed portfolio management.

")